Global hegemony and exorbitant privilege

How richness and winning go hand-in-hand, until they don’t

The gist: a new National Bureau of Economic Research paper draws the links between geo-financial advantage, geopolitical risk and national security of the United States, showing how they reinforce each other, but therefore how loss of financial advantage means security erodes too.

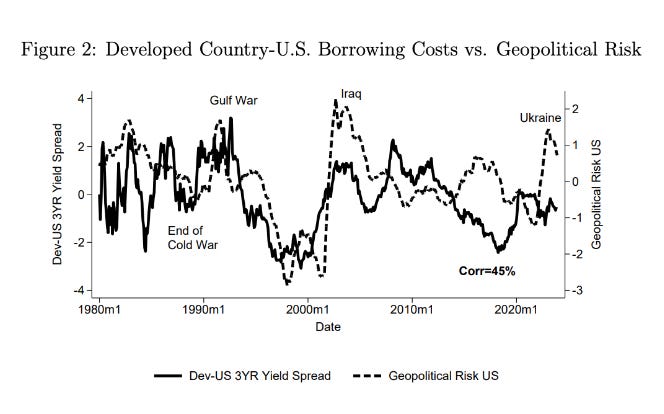

Periods of heightened geopolitical tension (dotted line) increases the United States’ borrowing advantage (solid line). Source https://www.nber.org/papers/w32775

We understand that it takes money to win wars. And that winning wars replenishes coffers, which makes for a reinforcing loop of military-financial supremacy, such as the US has enjoyed over the past 70 years and Great Britain did in the 19th Century, and every booty-winning country has since time began.

In a new National Bureau of Economic Research paper, Global Hegemony and Exorbitant Privilege, Carolin Pflueger (University of Chicago, Harris School of Public Policy) and Pierre Yared (Columbia Business School) draw the links at work in a more precise way: showing how military spending, geopolitical risk, and government bond prices are related and mutually determined.

In a dollar-based global economy the U.S. is able to borrow more cheaply than any competitor, a financial advantage which translates into borrowing for military spending power, and moreover, the research shows, this advantage increases with geo-political risk. The higher the global risk temperature, the more borrowing advantage the U.S. enjoys. This is because geopolitical upsets and periods of heightened tension increases the value of safe-haven US government debt value.

But why do we live in a dollar-based financial world? Because of military hegemony established post-war, and diligently asserted ever since. Borrowing advantage is created and maintained with arms. As Yared puts in on the CBS site, “Only a government with a very strong military can ensure that a country will most likely prevail and preserve the value of the assets it issues.”

So, maintaining global financial advantage is a matter of national security and vice versa, with global risk as a multiplier. This feedback loop works well, but also suggests how it all unravels: were the financial pre-eminence of the US as global bond currency to dissolve, so would its competitive advantage in military spending. (Of course, this does not factor in impoverishing its citizens to source the spend, but in theory, a diminished borrowing advantage erodes national offense and defense spending.)

In other words, what if, say, China successfully internationalizes the Renminbi as global reserve currency? The US would have to pay more to borrow from financial markets to maintain global military hegemony while China was able to compete for global capital on improved terms, leading to better terms on which to challenge that hegemony.

As with many economically based analyses which bracket out much to be able to focus on the connections between indicators, here massively important alternative drivers of change are left out: all kinds of questions of technology, innovation, not to mention social and cultural capital are conveniently filed in the “ceteris paribus” column. But, in its own terms, the study does put together a more deeply explanatory argument as to why financial hegemony is potentially the Achilles heel in US military supremacy.